For years, Fannie Mae and Freddie Mac have operated in a unique middle ground. They’ve never been fully government entities, but they also haven’t functioned as truly private companies since the 2008 financial crisis.

Since entering conservatorship under the Federal Housing Finance Agency, the mortgage industry has operated with a general understanding: liquidity would remain stable, underwriting standards would stay relatively consistent, and the broader system would continue functioning, even through market cycles.

That stability shaped the last decade and a half of mortgage lending.

Now, the conversation around privatization points to something much bigger than a policy shift. It has the potential to reshape how mortgage infrastructure is built, operated, and funded moving forward.

That matters far beyond Wall Street because it impacts lenders, capital markets, borrowers, and increasingly, the technology platforms powering modern lending.

The Backbone of the Mortgage Market

Fannie and Freddie sit at the center of the mortgage ecosystem.

They buy loans from lenders, standardize underwriting expectations, package mortgages into securities, and help create the liquidity that keeps the housing market moving. That process allows lenders to continue originating loans at scale without holding long-term risk on their balance sheets.

It’s also one of the main reasons the 30-year fixed-rate mortgage remains widely available in the U.S.

For years, conservatorship created a relatively stable operating environment. Capital continued flowing through the market, lending standards stayed consistent, and technology evolved around a framework lenders understood well.

Privatization changes some of the incentives behind that system and incentives tend to shape how markets behave.

Efficiency Suddenly Matters More

A more privatized structure creates a different kind of pressure across the industry.

Capital becomes more sensitive to performance, margins matter more, and operational efficiency becomes harder to ignore.

The mortgage industry has historically tolerated a surprising amount of operational friction. Manual reviews, duplicate data entry, disconnected systems, and fragmented workflows became part of the normal process over time.

In many ways, the broader market absorbed those inefficiencies. This becomes more difficult in an environment driven more directly by private capital expectations.

The conversation is no longer about whether digital transformation matters. Most lenders already know it does. The real question is whether existing systems can support the level of speed, consistency, and operational precision the next phase of the market may require.

Mortgage Technology Moves Deeper Into Operations

For the last decade, much of mortgage innovation focused on the borrower experience.

- Digital applications

- Mobile workflows

- Faster document uploads

- Cleaner front-end experiences

Those improvements still matter, but the next phase of mortgage technology is moving deeper into the operational side of lending.

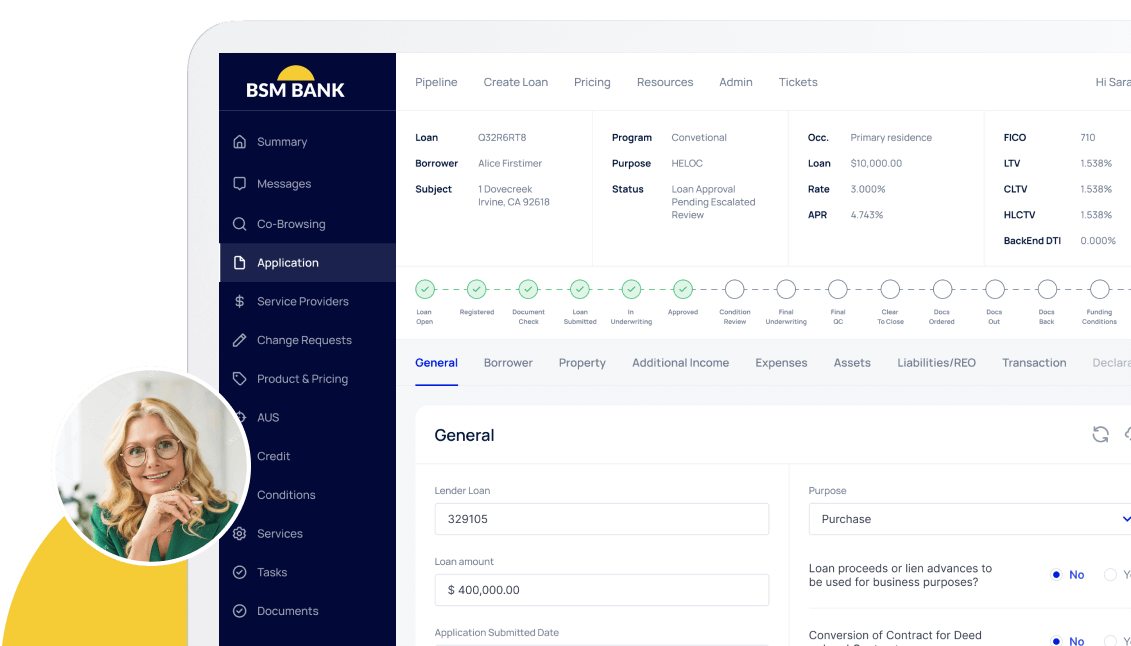

Underwriting workflows, data normalization, secondary market readiness, and internal process automation are becoming increasingly important. Lenders are paying closer attention to how information moves through the organization, how decisions are made, and how consistently loans can be produced at scale.

Artificial intelligence (AI) is accelerating that shift.

AI is starting to reshape income verification, risk analysis, document review, quality control, and underwriting consistency. The mortgage file itself is beginning to function less like a collection of documents and more like a connected dataset.

That transition has already been underway. Privatization simply increases the urgency around it.

The Rise of Lending Infrastructure Platforms

One of the biggest shifts happening across the industry has less to do with individual software products and more to do with the underlying infrastructure supporting lending itself.

For years, lenders built technology environments piece by piece.

- A point-of-sale (POS) from one vendor

- A loan origination system (LOS) from another

- Separate systems for documents, underwriting, compliance, servicing, workflow management, and analytics

Over time, many organizations ended up with disconnected systems tied together through integrations and manual workarounds.

Subscribe to BeSmartee 's Digital Mortgage Blog to receive:

- Mortgage Industry Insights

- Security & Compliance Updates

- Q&A's Featuring Mortgage & Technology Experts

That model becomes harder to sustain as the market demands greater efficiency, tighter margins, and faster decision-making.

This is where lending infrastructure platforms become increasingly important.

The industry is beginning to move away from standalone point solutions toward more unified platform architecture designed to support the full lending lifecycle.

We’re not talking about another mortgage POS or another commercial lending application, but a core technology layer capable of supporting:

- Workflow management

- Document management

- AI services

- Security and governance

- Borrower identity management

- Data orchestration

- Auditability

- Integration management

- Lifecycle management

In many ways, the mortgage industry is starting to follow the same path enterprise software followed years ago.

Platforms like Salesforce became successful not just because they offered software, but because they created configurable ecosystems companies could build operations around.

Lending technology is starting to evolve in a similar direction.

The future opportunity may not be building isolated products. It may be building connected infrastructure capable of supporting mortgage lending, commercial lending, underwriting intelligence, document automation, and workflow orchestration through a shared operational core.

That becomes even more important as AI adoption grows.

AI is only as effective as the systems supporting it. Fragmented infrastructure creates inconsistency, governance challenges, and operational risk. Enterprise-grade platforms create the foundation necessary for AI to operate reliably across lending workflows.

The larger opportunity is modernizing lending infrastructure itself.

A Bigger Divide Between Modernized and Fragmented Lenders

The mortgage industry has never operated on a completely level playing field.

Some lenders already have integrated systems and strong data governance. Others still rely heavily on disconnected workflows and manual operational processes.

A more performance-driven market makes that gap much more visible.

Lenders operating on modernized infrastructure gain advantages in speed, consistency, scalability, and loan quality. Lenders operating across fragmented systems face more friction, more operational cost, and slower execution.

This is especially important for community banks and credit unions.

Access to scalable infrastructure can help smaller lenders compete more effectively without needing enterprise-scale internal resources.

That creates an interesting dynamic where privatization could accelerate both consolidation and broader access to advanced lending technology at the same time.

The Industry Is Entering a Different Era

It’s easy to frame privatization as a political or regulatory conversation. But, it’s also an infrastructure conversation.

The mortgage market is gradually moving away from a system built around siloed workflows and document-heavy processes toward one centered on connected data, operational intelligence, and integrated technology ecosystems.

The conversation around privatization only accelerates the need for lenders to modernize faster.

And in the next phase of mortgage lending, the institutions with the strongest infrastructure may ultimately have the greatest advantage.