Speed has become one of the most talked-about priorities in commercial lending. Borrowers want answers quickly. Relationship managers want deals to move. Leadership wants shorter cycle times and higher throughput. On the surface, faster credit decisions feel like progress.

But speed alone doesn’t guarantee better outcomes.

In practice, many lenders discover that pushing for faster decisions without improving the quality and consistency of financial data can introduce new risks. Deals move quicker, but errors surface later. Credit committees spend more time debating numbers. Portfolio reviews become harder, not easier.

The real challenge isn’t choosing between speed and diligence. It’s ensuring that faster decisions are still grounded in accurate, standardized, and reliable financial analysis.

Key Insights at a Glance

- Faster decisions only add value when the underlying financial data is clean and consistent

- Rushed credit reviews often expose weaknesses in spreading and data preparation

- Manual financial prep is one of the biggest hidden bottlenecks to both speed and accuracy

- Inconsistent inputs create downstream risk for credit committees and portfolio management

- The most effective lenders combine automation with human judgment, not one or the other

Table of Contents

Why Speed Became the Priority

There’s a reason speed dominates lending conversations today. Competitive pressure is real. Borrowers compare lenders based on responsiveness. Referral partners expect quick feedback. Internally, teams are measured on turnaround times and pipeline velocity.

In response, many institutions focus on shaving days, or even hours, off the credit process. Some tighten SLAs. Others add staff. Some push analysts to “move faster” without changing the work itself.

That’s where problems begin. Speed targets applied to manual processes often create shortcuts. Analysts feel pressure to rush through data entry, reconciliation, or validation. Review layers compress. Assumptions go unchecked. The decision is faster, but the foundation is weaker.

When Faster Decisions Increase Risk

A fast credit decision built on inconsistent or incomplete data doesn’t reduce risk; it relocates it.

Common warning signs include:

- Credit committees questioning how ratios were calculated

- Analysts spending review time fixing numbers instead of assessing risk

- Inconsistent DSCR or cash flow logic across similar borrowers

- Portfolio teams struggling to compare borrowers year over year

- Audit findings tied to documentation or calculation inconsistencies

None of these issues stem from analysts lacking skill. They stem from manual, fragmented data preparation that wasn’t designed to scale under time pressure.

The Real Bottleneck Isn’t Underwriting

Many lenders assume underwriting itself is the slowest part of the process. In reality, the biggest delays often occur before underwriting truly begins.

Manual financial spreading is one of the most time-consuming stages in commercial lending. Analysts rekey figures from tax returns, reconcile discrepancies across schedules, apply adjustments, and rebuild spreadsheets, deal after deal.

When volume increases, this prep work becomes the constraint. Speeding up decisions without addressing this stage forces analysts to work faster in the least forgiving part of the process where accuracy matters most.

Why Clean Inputs Matter More Than Faster Outputs

Credit decisions are only as strong as the data behind them. When financial inputs vary by analyst, branch, or spreadsheet template, decision quality suffers.

Clean, standardized financial data enables:

- Faster reviews without rework

- More productive credit committee discussions

- Clearer trend analysis across borrowers and industries

- More reliable portfolio monitoring

- Stronger audit and compliance outcomes

Without consistency, speed creates friction instead of efficiency.

Where Automation Actually Helps

Automation doesn’t replace credit judgment. It improves the conditions under which judgment is applied.

Subscribe to BeSmartee 's Digital Mortgage Blog to receive:

- Mortgage Industry Insights

- Security & Compliance Updates

- Q&A's Featuring Mortgage & Technology Experts

Modern automation is most effective in the preparation phase, where it:

- Extracts financial data accurately from tax returns and statements

- Applies consistent classification and calculation logic

- Reduces manual rekeying and reconciliation

- Produces standardized spreads across borrowers

By removing repetitive prep work, analysts gain time to evaluate risk, assess trends, and apply experience, the parts of credit analysis that machines shouldn’t handle alone.

A Practical Balance: Speed With Structure

The most effective lenders don’t chase speed for its own sake. Instead, they focus on building workflows where speed is a natural outcome of better structure, cleaner inputs, and clearer accountability.

In these environments, analysts are no longer pressured to rush through data preparation just to meet turnaround targets. Credit teams spend less time debating how numbers were calculated and more time evaluating what those numbers actually mean. Review cycles shorten not because steps are skipped, but because fewer corrections and clarifications are needed downstream.

This approach also creates resilience during volume spikes. When loan demand increases, structured processes scale far more effectively than manual ones. Rather than overwhelming staff or introducing inconsistency, lenders with standardized data workflows can absorb higher volumes while maintaining decision quality. Speed, in this context, becomes sustainable rather than fragile.

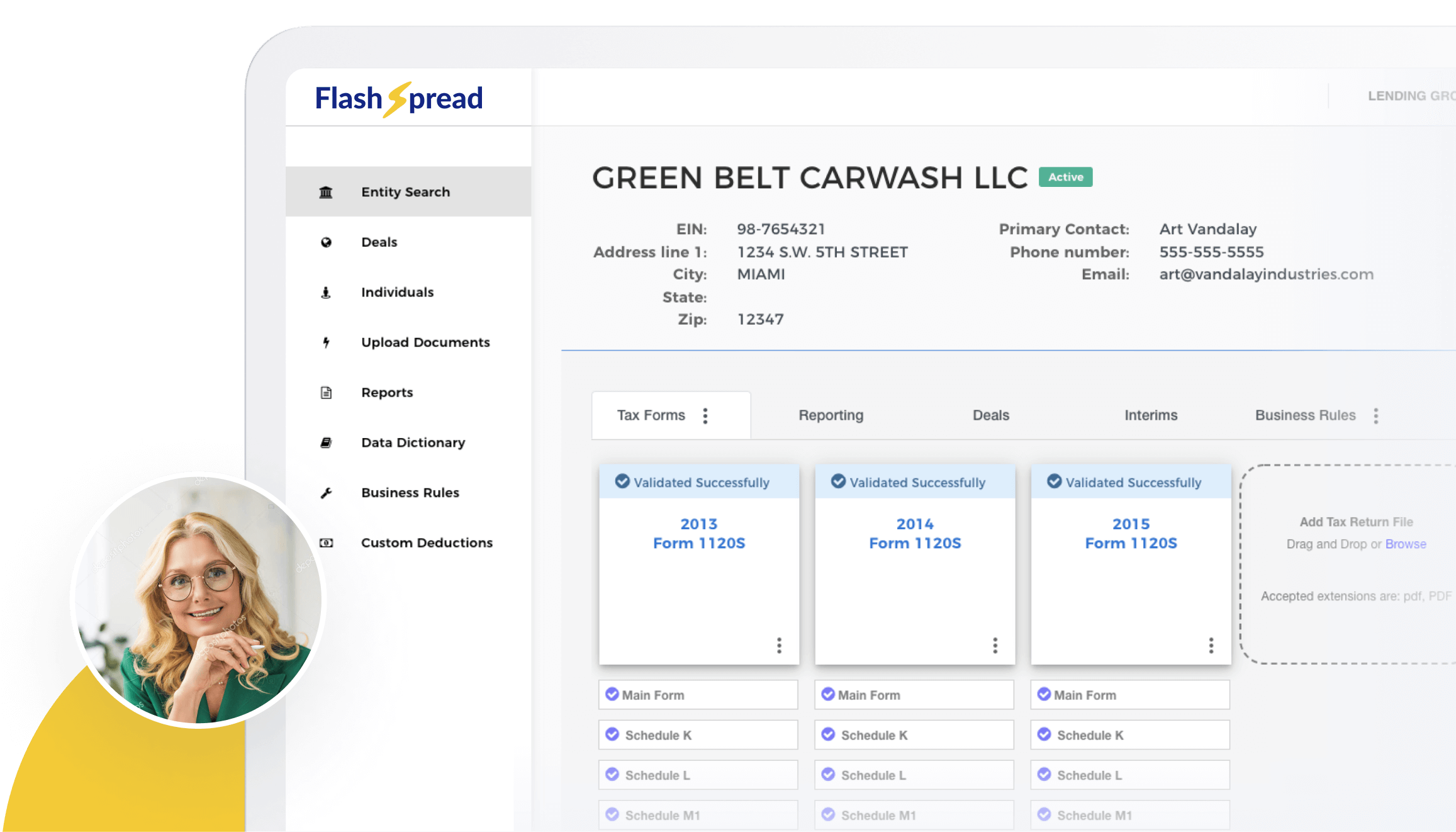

How Tools Like FlashSpread Support Better Decisions

One way lenders strengthen the balance between speed and sound judgment is by improving how financial data is prepared before underwriting begins.

FlashSpread is designed to automate the financial spreading stage for commercial and SBA lending teams, using OCR combined with machine learning to extract and organize data from tax returns and financial statements, including scanned documents, in minutes instead of hours.

In practice, this supports better decisions by:

- Reducing manual data entry: Financial data is extracted and spread automatically, limiting rekeying and reconciliation work.

- Improving accuracy and consistency: Standardized spreads and calculation logic help reduce analyst-by-analyst variation.

- Speeding up preparation, not judgment: Analysts receive structured data faster, allowing more time for interpretation and risk assessment.

- Supporting complex workflows: Global debt service calculations and structured outputs help teams evaluate borrower health more efficiently.

- Producing audit-ready data: Clean, consistent spreads make reviews and validations easier downstream.

Rather than accelerating decisions at the expense of quality, tools like FlashSpread focus on strengthening the foundation of the credit process, so faster decisions are also more reliable.

Q&A: Common Questions About Speed and Credit Quality

Q: Doesn’t faster decisioning automatically improve borrower experience?

A: Only if decisions are accurate and consistent. Borrowers feel friction when deals stall later due to rework or clarification requests.

Q: Can automation really reduce risk while increasing speed?

A: Yes, when it standardizes data preparation and reduces manual errors. Automation strengthens the foundation of the decision, not the judgment itself.

Q: Is slowing down ever the right answer?

A: Not necessarily. Improving structure and inputs often delivers both speed and accuracy without sacrificing either.

Roundup

Faster credit decisions aren’t inherently better; better credit decisions are. When speed is pursued without addressing manual prep work and inconsistent financial data, risk often increases even as timelines shrink.

Lenders seeing the strongest outcomes focus on improving how financial information is prepared before underwriting begins. Clean, standardized inputs allow analysts to move faster with confidence, reduce friction in reviews, and support clearer portfolio oversight.

By pairing automation for data preparation with human expertise for interpretation, lenders can achieve decisions that are both timely and sound, even as volume and complexity grow.

Want faster credit decisions that still stand up to review? Learn how structured spreading supports better outcomes.