Many lenders still wonder whether automation can accurately process both income statements and balance sheets, and it’s an understandable question. Early digital tools weren’t built to interpret complex financials or mixed document types, which left room for error and inconsistency. Analysts often remember manually reconciling income statements and balance sheets, flipping back and forth between PDFs and Excel, and worrying whether totals and ratios matched across documents.

But today’s automation capabilities tell a very different story. Modern solutions not only extract numbers accurately but also normalize and structure them for consistent analysis. This eliminates human error and dramatically reduces manual workload.

In this post, we’ll clear up the misconception, explain why these limitations exist, and show how modern automation, including tools with a small AI component, makes working with both types of financial statements faster, cleaner, and more reliable.

Key Insights at a Glance

- Misunderstandings about statement handling often come from legacy tools, not current technology.

- Many LOS systems collect financials but don’t analyze them, leaving manual gaps.

- Automation can extract, normalize, and structure both income statements and balance sheets efficiently.

- Standardized data allows lenders to spread more deals without extra manual effort.

- Reducing manual preparation helps credit teams focus on risk analysis and portfolio decisions.

- Automation enhances consistency across analysts and branches, avoiding discrepancies in calculations.

- Properly implemented workflows maintain borrower trust while speeding up decision-making.

Table of Contents

Why This Misconception Exists

For years, lenders used manual or semi-automated tools that could handle only partial data, such as income statements but not full balance sheets.

This created a lasting assumption: automation can’t interpret both document types accurately. In truth, the problem was never with the financials themselves but with limitations in early OCR tools, rigid mapping, and inflexible templates. Analysts were still required to reconcile totals manually, ensure ratio consistency, and validate classification of line items like Schedule C, K-1, or 1120-S forms.

Today’s automation platforms process financials as a complete set, linking income statements, balance sheets, and supporting schedules into one cohesive view. But the misconception persists, especially among teams that have only seen older systems in action.

Many institutions are still running on legacy workflows that “digitize” the process without transforming it. Documents may move faster through the pipeline, but the data inside them remains locked in PDFs until someone rekeys it. These outdated steps give the illusion of automation, when in reality, analysts are still performing the same manual work under a different label.

Expanding awareness of what automation can do helps lenders make smarter decisions, reduce processing times, and maintain accuracy across the entire portfolio.

Where the LOS Leaves Off

Loan origination systems (LOS) are designed primarily for document intake and workflow tracking, not for financial interpretation.

- Once financial documents are uploaded, they often sit in the system until an analyst intervenes.

- Analysts must open PDFs, scroll through tax returns, and extract numbers line by line.

- Numbers are then retyped into spreadsheets or internal templates, a slow process prone to errors.

- Each analyst may calculate ratios slightly differently, adding inconsistency across files.

- Narratives and memos summarizing borrower performance are typically written manually, creating variation in commentary tone.

This manual layer is where inefficiency hides. Even though the LOS appears automated, real spreading and ratio calculation remain human-driven, which is why some lenders doubt automation’s ability to handle complex statements.

In many lending teams, this “invisible manual gap” becomes a scalability barrier. As loan volumes rise, analysts can’t simply type faster to keep up. The more documents they manage, the higher the risk of errors, duplicate data entry, or inconsistent interpretations. Over time, this slows credit decisions, inflates review workloads, and makes it difficult to maintain uniform risk standards across the organization.

By understanding these gaps, lenders can identify exactly where automation is most valuable before analysts spend hours on repetitive tasks that don’t require judgment.

Bridging the Gap With Smarter Spreading Automation

Modern automation doesn’t replace analysts; it augments them. It reduces time spent on repetitive tasks while allowing credit teams to focus on analysis, risk evaluation, and borrower engagement.

Subscribe to BeSmartee 's Digital Mortgage Blog to receive:

- Mortgage Industry Insights

- Security & Compliance Updates

- Q&A's Featuring Mortgage & Technology Experts

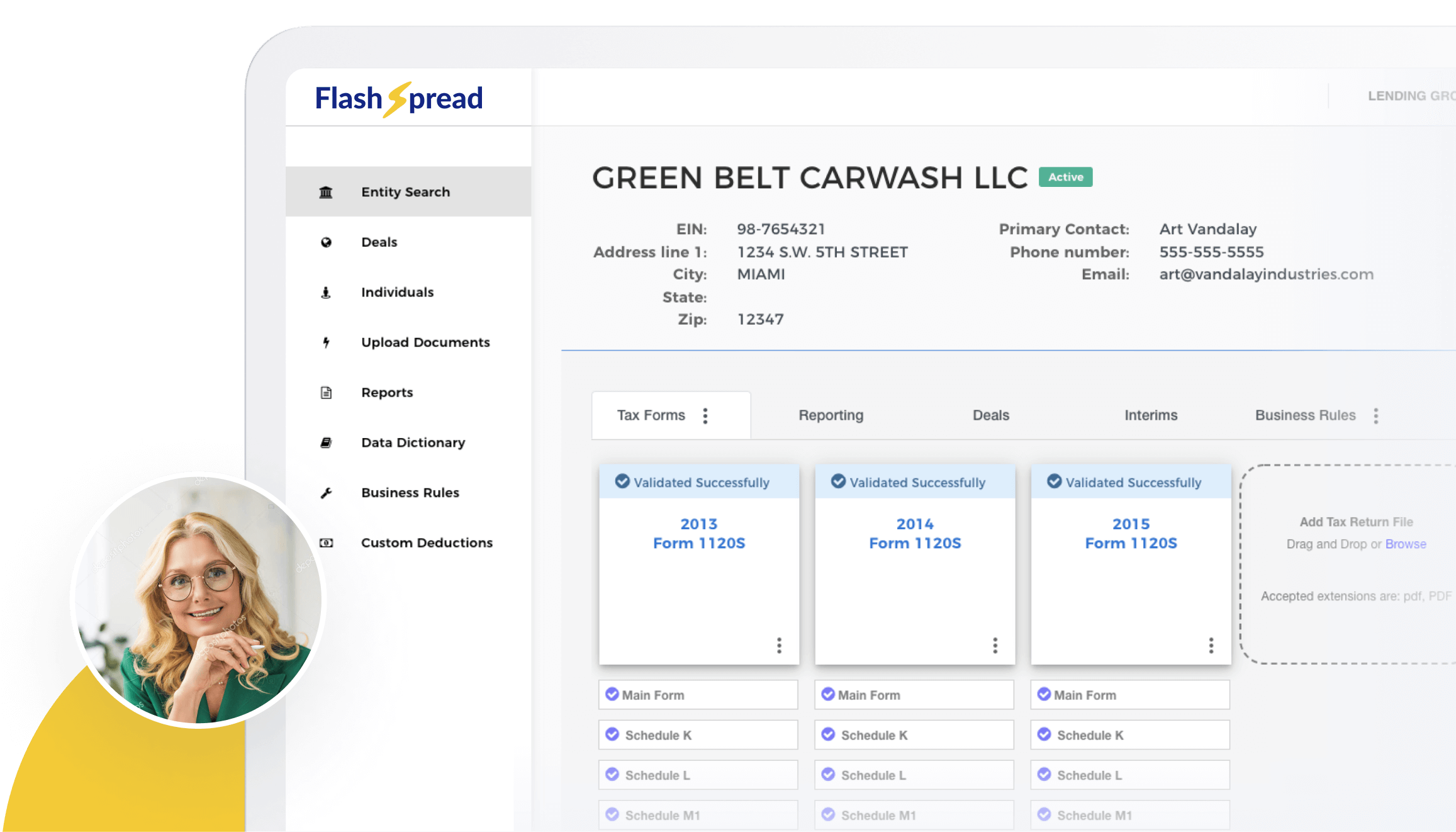

FlashSpread is an example of a tool designed to address this exact workflow gap.

- Using OCR (optical character recognition) and machine learning, FlashSpread extracts and organizes complex data from tax returns, income statements, and balance sheets, even when scanned or handwritten.

- The system spreads data for underwriters to apply KPIs instantly, reducing spreading time from roughly three hours to under five minutes.

- Built-in intelligence automatically classifies line items, flags potential anomalies, and suggests ratio adjustments for review.

- Each spread follows a standardized, transparent structure, ensuring cross-borrower comparability.

- Analysts no longer need to reconcile totals or copy data between templates; reports are generated instantly and can be exported directly into credit packages.

- The tool integrates seamlessly with LOS workflows, so lenders can push tax returns directly to FlashSpread and receive structured data back into their system.

FlashSpread is currently enhancing its beta capabilities to analyze both personal and business financials, including affiliate entities. This enables lenders to evaluate borrower health holistically, not in isolation. The result is faster underwriting, improved accuracy and greater confidence in every decision, all without expanding headcount.

By bridging the gap between LOS intake and financial analysis, automation solves the exact objection lenders often raise: “Can it handle both income statements and balance sheets?” The answer is yes and today, it’s being done faster, more consistently, and with better audit trails than ever before.

Quick Q&A: Addressing the Top 3 Lender Questions

Q. Can automation really process both income statements and balance sheets?

A. Yes. Modern OCR automation accurately captures and maps both, ensuring consistency between related accounts.

Q. Does it work with PDFs and scanned documents?

A. Absolutely. It’s designed for real-world submissions: tax returns, scans, even handwritten notes.

Q. Will it integrate with my LOS?

A. Yes. Spreading automation complements LOS workflows, closing the gap between document intake and financial analysis.

Roundup

For many lenders, questions about income statements and balance sheets reflect a wider concern about trust and reliability in automation.

Legacy systems could not consistently handle complex, multi-document spreads, but modern automation platforms have evolved. By reducing manual reconciliation, standardizing line items, and leveraging small AI components to classify and check data, lenders can now process complete financial statements efficiently.

The benefits go beyond speed: analysts spend less time on repetitive tasks and more on portfolio insights and risk evaluation. Borrowers receive faster, more consistent outcomes, which improves experience and satisfaction.

Automation closes the workflow gap that created the misconception in the first place. When a LOS collects the documents and automation completes the spreading, lenders can finally say with confidence: “Yes, we handle income statements and balance sheets too.”

If you’ve ever wondered whether automation can truly handle both, the answer is yes. Discover how modern financial spreading brings clarity to complex borrower data.