Mortgage delinquencies have been a persistent concern in the housing market, reflecting the broader economic challenges and financial health of homeowners across the United States. Over the last ten years, the landscape of mortgage delinquencies has seen dramatic shifts, influenced by economic downturns, recovery phases, and unexpected global events like the COVID-19 pandemic. According to the Mortgage Bankers Association, the national mortgage delinquency rate spiked to 8.22% in the second quarter of 2020 during the height of the pandemic—a stark contrast to the decade-low rate of 3.36% recorded just a year earlier in 2019.

Understanding these fluctuations and the factors driving them is crucial for homeowners, lenders, and policymakers alike. In this blog post, we will explore the key trends and factors that have shaped mortgage delinquencies over the past decade and how they continue to impact the market today.

Table of Contents

Understanding Mortgage Delinquencies

Mortgage delinquency occurs when borrowers fail to make their monthly payments on time. Delinquencies are typically categorized by how many days a payment is overdue: 30, 60, 90 days, or more. The severity increases with time, and if left unresolved, delinquencies can lead to foreclosure, where the lender takes possession of the property to recover their losses.

The rate of mortgage delinquencies is a crucial indicator of the health of the housing market and the overall economy. High delinquency rates signify economic distress, whereas low rates suggest financial stability and robust market conditions.

The Last Decade: A Snapshot of Mortgage Delinquencies

Over the past decade, mortgage delinquencies have fluctuated due to various economic, social, and regulatory factors. Let’s examine the key events and trends shaping mortgage delinquencies from 2014 to 2024.

1. The Aftermath of the Great Recession (2014-2015)

The early part of the last decade was still heavily influenced by the aftershocks of the 2008 financial crisis. Although the crisis had officially ended, its ripple effects were felt for years, particularly in the housing market. Mortgage delinquencies were elevated in 2014 and 2015 as many homeowners struggled to recover from job losses, declining home values, and underwater mortgages (where the loan amount is higher than the property’s market value).

During this period, government intervention through programs like the Home Affordable Modification Program (HAMP) helped reduce delinquency rates by offering loan modifications to distressed homeowners. The unemployment rate was also steadily declining, contributing to a gradual improvement in delinquency rates.

2. Economic Recovery and Stabilization (2016-2019)

From 2016 to 2019, the U.S. economy experienced growth and stabilization. Unemployment rates fell to record lows, and wage growth, although modest, began to pick up. The housing market benefited from these favorable economic conditions, and mortgage delinquencies steadily decreased.

Lenders also implemented stricter lending standards post-2008, reducing the number of high-risk loans. As a result, the proportion of loans entering delinquency declined. The mortgage delinquency rate reached a historic low in early 2019, reflecting a strong economy and a more cautious lending environment.

3. The Impact of COVID-19 (2020-2021)

The onset of the COVID-19 pandemic in early 2020 brought unprecedented challenges to the housing market. Unemployment rates soared as businesses closed or reduced operations due to lockdowns and social distancing measures. Many homeowners found themselves unable to keep up with their mortgage payments, leading to a sharp increase in delinquencies.

However, this time, the government and financial institutions quickly acted. Programs like the Coronavirus Aid, Relief, and Economic Security (CARES) Act temporarily relieved millions of homeowners through mortgage forbearance options. These measures allowed borrowers to pause their mortgage payments without penalty, which helped prevent a wave of foreclosures.

The intervention was largely successful, and while there was a notable spike in delinquencies during the pandemic’s peak, the rates began to decline again as the economy gradually reopened and employment rates improved.

Subscribe to BeSmartee 's Digital Mortgage Blog to receive:

- Mortgage Industry Insights

- Security & Compliance Updates

- Q&A's Featuring Mortgage & Technology Experts

4. Post-Pandemic Recovery and Current Trends (2022-2024)

As the economy began recovering from the pandemic, mortgage delinquencies declined throughout 2022 and 2024. However, the landscape had its challenges. Rising inflation, interest rates, and housing prices put pressure on new and existing homeowners, potentially increasing their risk of delinquency.

In 2023, delinquencies remained relatively low compared to the post-recession period. Still, there were signs of potential stress in the market. Economic uncertainties, such as geopolitical tensions and fluctuating energy prices, could impact borrowers’ ability to maintain their mortgage payments. Additionally, the end of mortgage forbearance programs meant that some homeowners were now dealing with the accumulation of deferred payments.

Key Factors Influencing Mortgage Delinquencies

Several factors have played significant roles in influencing mortgage delinquency rates over the past decade:

- Economic conditions: Employment rates, wage growth, and economic stability are critical factors influencing a homeowner’s ability to make timely mortgage payments. Economic downturns often lead to higher delinquency rates.

- Interest rates: The cost of borrowing is directly affected by interest rates. Higher rates can lead to increased monthly payments for adjustable-rate mortgages (ARMs), making it harder for some borrowers to stay current.

- Housing market dynamics: Home prices and their stability impact homeowners’ equity and ability to refinance or sell in a pinch. Sharp declines in home values can lead to higher delinquencies, particularly for those with little equity.

- Government policies and interventions: Policies that provide relief during economic crises, such as mortgage forbearance or modification programs, directly impact delinquency rates.

- Lending standards: Stricter lending standards post-2008 have generally reduced the number of risky loans, leading to fewer delinquencies. However, economic pressures can still influence even the most qualified borrowers.

The Role of Technology in Mitigating Delinquencies

Over the past decade, the rise of digital solutions has transformed the mortgage industry by leveraging technology to streamline the entire process, increase transparency, and provide a better borrower experience. These advancements have played a crucial role in reducing delinquency rates by enabling more accurate risk assessments, faster loan processing, and clearer communication between lenders and borrowers, ultimately leading to more informed decisions and fewer missed payments.

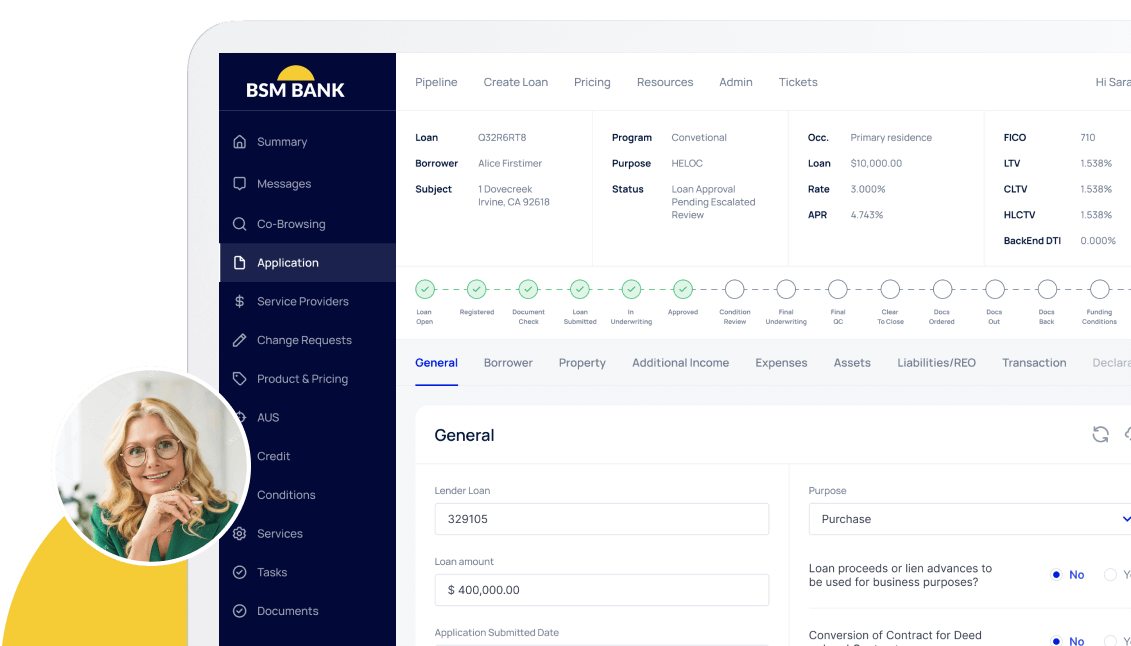

BeSmartee’s mortgage product suite has been at the forefront of this transformation. By providing a seamless, user-friendly interface that simplifies the mortgage application process, BeSmartee helps borrowers better understand their financial commitments and select mortgage products that align with their financial situation. Additionally, when integrated with other systems like Encompass, a widely used loan origination system (LOS), the mortgage process becomes even more efficient.

Encompass streamlines loan processing and underwriting, while BeSmartee enhances the borrower experience on the front end, resulting in smoother workflows, faster approvals, and better coordination between borrowers and lenders. Together, these systems create a comprehensive digital ecosystem that reduces errors, improves transparency, and ultimately helps reduce delinquency rates.

Looking Ahead: What to Expect in the Coming Years

As we look to the future, economic, social, and technological factors will continue influencing mortgage delinquencies. While the current environment suggests a relatively stable outlook, potential challenges such as economic slowdowns, rising interest rates, and geopolitical tensions could create new stress points for homeowners.

It will be crucial for lenders, policymakers, and homeowners to remain vigilant and proactive in managing these risks. Leveraging technology, like Bright POS and Bright Connect, can play a pivotal role in helping all stakeholders navigate these uncertainties more effectively.

Conclusion

The last decade has seen significant fluctuations in mortgage delinquencies, driven by economic shifts, regulatory changes, and unprecedented events like the COVID-19 pandemic. As we move forward, understanding these trends and their underlying causes will be essential for managing future risks in the housing market.

With BeSmartee’s innovative digital solutions, lenders can streamline the mortgage process from application to closing, ensuring a more efficient and transparent workflow. Contact us today to learn how BeSmartee can help you optimize your lending operations, minimize the risk of delinquencies, and stay competitive in an evolving market. Let BeSmartee support your path to success in the mortgage industry!