Many lending organizations eventually evaluate whether they need a Loan Origination System (LOS). As teams grow, processes become more complex, loan volumes increase, and leaders begin looking for ways to improve efficiency across the lending operation.

For some institutions, an LOS is absolutely the right investment. These platforms help manage applications, workflows, approvals, borrower information, and operational processes throughout the lending lifecycle.

But many lenders discover something interesting during that evaluation process: their biggest bottlenecks are not always happening in origination.

They are happening before underwriting can begin.

Analysts are still spending hours extracting data from borrower documents, building spreads, validating financials, and preparing information for review. Even when application and workflow management are functioning well, the work required to transform borrower documents into usable financial data often remains highly manual.

This is one reason many lenders choose to modernize credit workflows before making a larger LOS investment.

Key Insights at a Glance

- A LOS and a core credit workflow solve different operational challenges

- Many lending bottlenecks occur before underwriting begins

- Manual spreading remains one of the most time-intensive credit tasks

- Modernizing financial data preparation can improve throughput and consistency

- Structured financial data supports underwriting, reporting, and monitoring

- FlashSpread helps lenders reduce manual spreading and prepare decision-ready financial data faster

Table of Contents

Loan Origination and Credit Preparation Serve Different Purposes

A common misconception is that every lending challenge can be solved through a single platform.

In reality, loan origination and credit preparation address different operational needs.

An LOS helps manage how loans move through the organization. It supports application intake, workflow routing, approvals, borrower management, and operational oversight.

Credit preparation focuses on something different: turning borrower documents into financial information that can be analyzed and used for underwriting.

Before a credit decision can occur, lenders often need to:

- Review borrower documents

- Extract financial information

- Build spreads

- Validate results

- Standardize financials

- Prepare underwriting-ready analysis

For many organizations, these activities remain among the most manual parts of the lending process.

Why Credit Teams Still Feel Bottlenecks

Many lenders assume that growth challenges are primarily caused by underwriting capacity.

In reality, analysts often spend significant time preparing information before credit analysis begins.

A typical workflow may include:

- Reviewing tax returns

- Reviewing financial statements

- Extracting financial values

- Rekeying information into spreadsheets

- Validating calculations

- Organizing supporting documentation

None of this work directly improves credit judgment.

It creates the foundation required for credit judgment.

As loan volume increases, this preparation work grows as well. More borrowers create more documents. More documents create more extraction, validation, and spreading work.

The result is that analyst capacity becomes constrained long before underwriting expertise becomes the limiting factor.

Why Adding More Analysts Is Not Always the Answer

When deal volume increases, lenders often respond by hiring more staff.

That can provide temporary relief, but it does not fundamentally change the workflow.

The underlying process remains dependent on people manually preparing financial data before underwriting can begin.

This creates a scaling challenge:

Subscribe to BeSmartee 's Digital Mortgage Blog to receive:

- Mortgage Industry Insights

- Security & Compliance Updates

- Q&A's Featuring Mortgage & Technology Experts

- More deals require more document review

- More document review requires more analyst effort

- More analyst effort requires more headcount

The relationship becomes largely linear.

Many lending organizations are now looking for ways to improve throughput without increasing staffing requirements at the same pace as loan growth.

The Gap Between Borrower Documents and Underwriting

Most lending technology is designed to help manage information after it has already been prepared.

The challenge is that borrower financial data often arrives in formats that are not immediately usable.

Tax returns, financial statements, rent rolls, debt schedules, and supporting documents may all contain valuable information, but someone still needs to organize and prepare that information before underwriting can begin.

This creates a gap between document collection and credit analysis.

For many lenders, that gap remains highly manual even when other parts of the lending operation are supported by technology.

As a result, teams continue to spend significant time preparing data instead of evaluating risk.

Why Some Lenders Start With Credit Workflow Modernization

Rather than beginning with a broader platform initiative, many lenders focus first on improving the most labor-intensive parts of the credit process.

The objective is straightforward:

Reduce the manual work required to prepare borrower information for analysis.

When financial data can be extracted, standardized, and organized more efficiently, teams can:

- Increase analyst productivity

- Improve consistency across reviews

- Reduce rework

- Accelerate underwriting preparation

- Support future growth without proportional staffing increases

This creates operational improvements regardless of whether a lender ultimately adopts a LOS later.

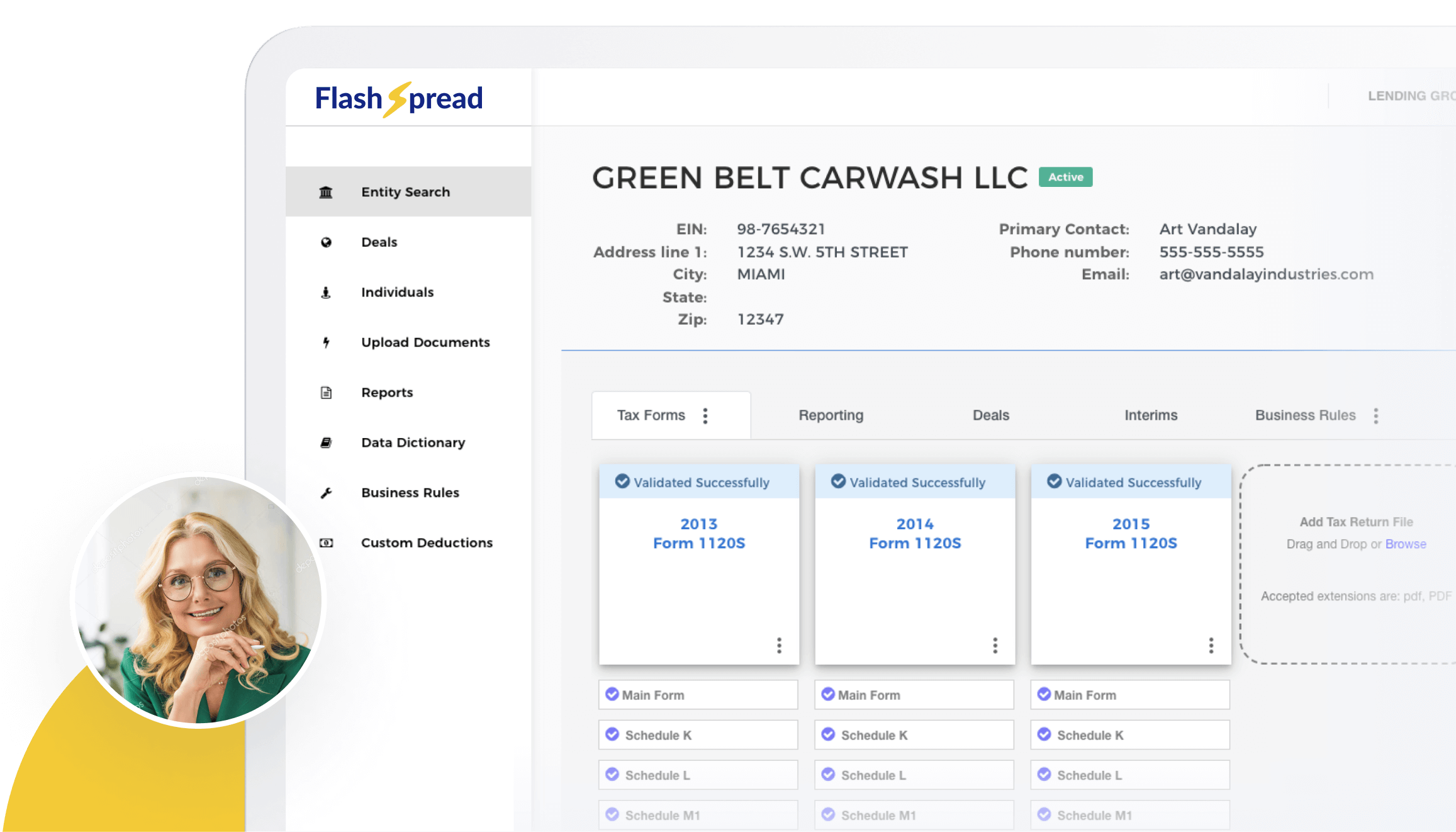

How FlashSpread Fits

FlashSpread helps lenders modernize the work that occurs between borrower documents and underwriting.

Using OCR, machine learning, and AI-enabled extraction, FlashSpread reads borrower documents such as tax returns, financial statements, and supporting financial files. It extracts and organizes financial data into standardized spreads and decision-ready outputs.

With FlashSpread, credit teams can:

- Reduce manual extraction and rekeying

- Create more consistent financial spreads

- Improve analyst productivity

- Accelerate underwriting preparation

- Generate structured financial data for downstream workflows

Once financial information is structured, it can support underwriting, credit memo preparation, reporting, portfolio monitoring, dashboards, and future credit intelligence initiatives.

The goal is not to replace every system a lender uses. It is to reduce the manual work required to prepare financial data and create a stronger foundation for the credit process.

Roundup

A LOS can be an important part of a lending technology strategy, but it does not automatically eliminate the manual work that occurs before underwriting begins.

For many lenders, one of the largest opportunities for improvement exists in the credit workflow itself. Manual spreading, financial data preparation, and document review continue to consume valuable analyst time and can limit scalability as loan volume grows.

That is why many organizations are focusing on credit workflow modernization first. By reducing manual spreading and improving how borrower financial data is prepared, lenders can increase throughput, improve consistency, and build a stronger foundation for future technology initiatives.

If your team is still spending hours preparing borrower financials before underwriting can begin, it may be time to evaluate the credit workflow itself. See how FlashSpread helps lenders reduce manual spreading and prepare decision-ready financial data faster.