Commercial lenders often focus on improving underwriting speed, but one of the biggest bottlenecks occurs before underwriting ever begins.

Analysts spend hours extracting data from tax returns, financial statements, rent rolls, debt schedules, and supporting borrower documents. Before a credit decision can be made, someone must locate key figures, rekey data into spreadsheets, standardize financials, calculate ratios, and validate results.

This work is necessary, but it does not create credit insight. It creates credit readiness.

As loan volumes increase, many lenders discover that their real constraint is not underwriting capacity. It is the manual effort required to prepare borrower data for analysis.

Key Insights at a Glance

- Manual spreading slows credit teams before underwriting begins

- Analysts spend valuable time extracting, rekeying, and validating borrower data

- More loan volume often creates more manual preparation work

- AI-enabled extraction helps reduce repetitive document processing

- Structured financial data supports underwriting, reporting, monitoring, and future credit workflows

- FlashSpread helps lenders move from borrower documents to decision-ready financial data faster

Table of Contents

The Hidden Cost of Data Preparation

When people discuss credit workflows, the conversation often focuses on underwriting decisions. Yet much of an analyst’s day is spent preparing information rather than evaluating risk.

A typical workflow looks like this:

- Borrower submits financial documents as PDFs

- Analyst reviews and extracts data

- Financials are rekeyed into spreadsheets

- Data is standardized and categorized

- Ratios are calculated and validated

- Underwriting begins

Each step adds time, introduces opportunities for inconsistency, and limits how many deals a team can process.

The challenge is not Excel itself. Spreadsheets remain valuable for modeling, sensitivity analysis, and review. The challenge is using spreadsheets as the primary mechanism for converting unstructured borrower documents into usable financial data.

Why More Analysts Is Not a Long-Term Solution

When credit volumes rise, lenders often respond by adding staff.

While that may increase capacity temporarily, it does not address the underlying issue. More deals create more documents. More documents create more manual extraction work. More manual extraction creates additional opportunities for delays, inconsistencies, and rework.

This creates a linear scaling problem: growth requires proportionally more analyst effort.

Modern lending organizations are increasingly looking for ways to break that relationship by reducing the amount of manual work required before underwriting begins.

The Shift From Document Processing to Data Processing

The most significant change occurring in commercial lending is not better spreadsheets. It is the ability to transform borrower documents into structured financial data automatically.

Instead of relying on analysts to manually extract and organize information, AI-enabled extraction can identify key financial values directly from borrower documents and convert them into standardized data.

The workflow changes from:

PDF to Analyst to Spreadsheet to Underwriting

to:

PDF to AI Extraction to Structured Financial Data to Underwriting

This shift allows analysts to focus on reviewing exceptions, identifying trends, and exercising credit judgment rather than performing data entry.

Subscribe to BeSmartee 's Digital Mortgage Blog to receive:

- Mortgage Industry Insights

- Security & Compliance Updates

- Q&A's Featuring Mortgage & Technology Experts

Why Structured Data Matters

The immediate benefit of automation is time savings. The longer-term benefit is creating a reusable financial data foundation.

Once borrower information exists as structured data, it can support:

- Financial spreading

- Underwriting workflows

- Credit memo generation

- Portfolio monitoring

- Management reporting

- Dashboarding and analytics

- Future AI-assisted credit tools

Rather than recreating the same information in multiple systems, lenders can use a single source of financial data throughout the credit lifecycle.

This improves consistency, reduces rework, and creates greater visibility across the organization.

The goal is not simply to create spreads faster. It is to create a foundation for more connected credit workflows. Once borrower financial data is structured, lenders can use it across underwriting, reporting, monitoring, and tools like AskFlash that help teams access credit guidance and institutional knowledge through source-cited responses.

Structured Data Creates Value Beyond the Spread

Once borrower information has been extracted and standardized, its value extends far beyond the initial spread.

Traditionally, financial data often becomes trapped within individual spreadsheets, making it difficult to reuse across the credit process. Analysts, underwriters, and reviewers may spend time locating information, recreating calculations, or validating data that already exists elsewhere.

When financial information is structured from the start, it can flow more easily into underwriting, credit memos, reporting, portfolio monitoring, and other downstream processes.

This creates several benefits:

- Greater consistency across borrowers and analysts

- Reduced rework and duplicate effort

- Faster preparation for underwriting review

- Easier reporting and portfolio analysis

- Improved visibility across the credit lifecycle

The immediate benefit is faster spreading. The broader benefit is creating a standardized financial data foundation that can support multiple workflows without requiring teams to repeatedly rebuild the same information.

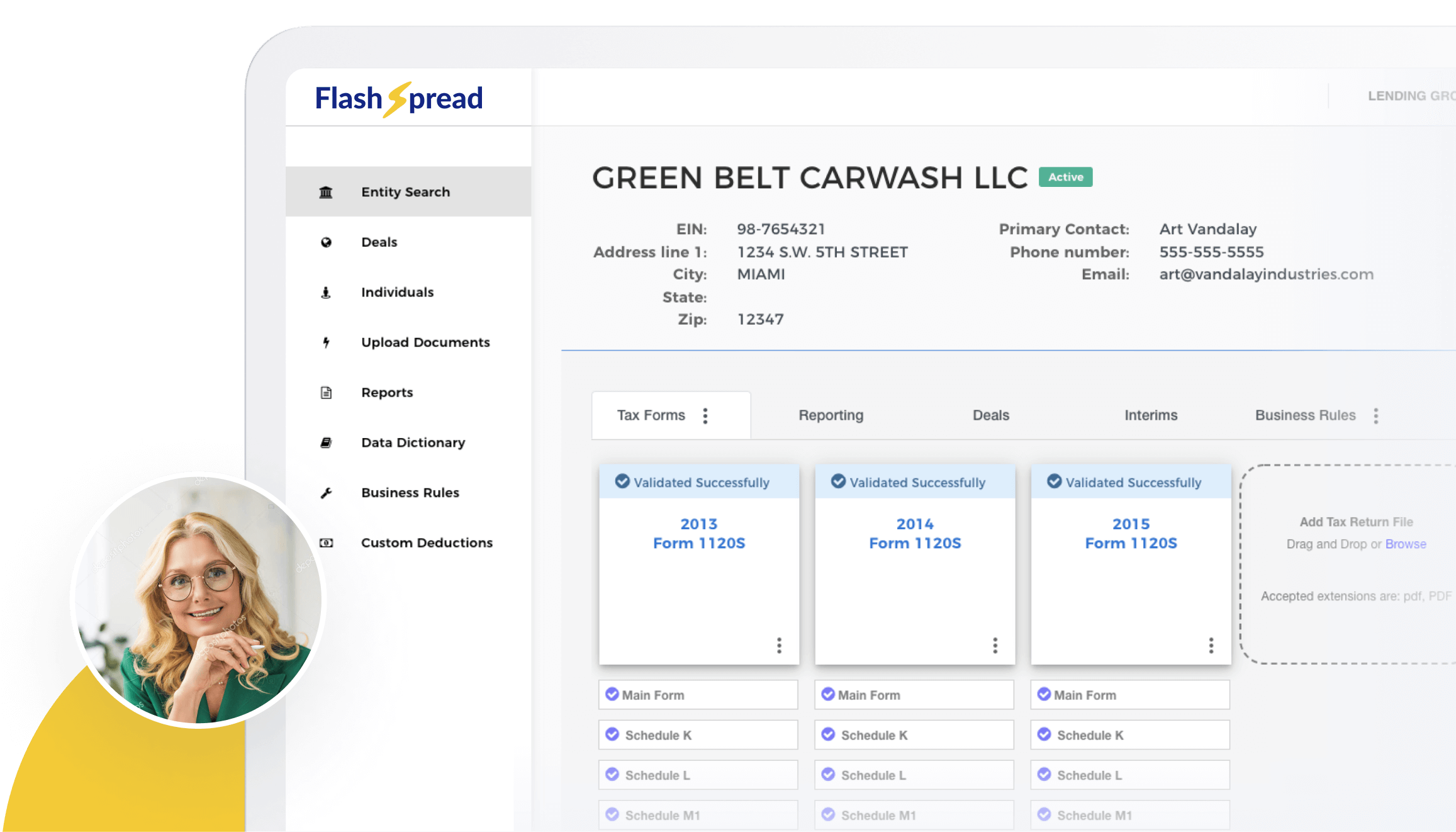

How FlashSpread Helps

FlashSpread helps lenders move from borrower documents to decision-ready financial data faster.

Using OCR, machine learning, and AI-enabled extraction, FlashSpread reads financial statements, tax returns, and supporting borrower documents, automatically extracting and organizing financial data into standardized spreads.

The result is not simply a faster spreading process. It is a more scalable credit workflow that allows analysts to spend more time evaluating risk and less time preparing data.

For lenders looking to increase throughput, improve consistency, and build a stronger foundation for future credit technology initiatives, reducing manual spreading may be one of the highest-impact opportunities available today.

Roundup

Commercial lending teams do not gain a competitive advantage from manually moving numbers from PDFs into spreadsheets.

Their advantage comes from how effectively they evaluate risk, serve borrowers, and make credit decisions.

The organizations that scale most effectively will be those that spend less time preparing financial data and more time using it.

If your analysts are still spending hours preparing borrower data before underwriting can begin, it may be time to rethink the workflow. See how FlashSpread helps lenders reduce manual spreading and move from borrower documents to decision-ready financial data faster.