Commercial lenders invest heavily in pipeline growth. Marketing budgets expand. Relationship managers are incentivized to source more deals. Intake processes are refined. Deal sourcing and referral networks are expanded.

Yet despite stronger front-end activity, many institutions struggle to translate pipeline growth into funded volume.

The reason often lies downstream.

In commercial lending, the real constraint is not intake velocity. It is the decision velocity. And decision velocity lives inside the credit desk. This blog explores the difference between pipeline velocity and decision velocity, where analysts lose time today, and how structured financial spreading and underwriting intelligence can transform the credit desk from an operational cost center into a growth lever.

Key Insights at a Glance

- Pipeline growth does not automatically translate to funded growth

- Decision velocity determines whether revenue converts

- Credit desks absorb complexity hidden from pipeline activity

- Manual spreading and policy interpretation create rework loops

- Structured financial data reduces friction and accelerates approvals

- Underwriting intelligence supports growth without lowering standards

Pipeline Velocity vs. Decision Velocity

In most lending institutions, pipeline velocity receives significant attention. The following metrics are tracked closely:

- Lead generation volume

- Application submissions

- Referral conversion rates

- Time to submission

However, once a deal reaches underwriting, a different dynamic takes over. The focus shifts from volume to evaluation. Credit risk must be assessed. Financial documents must be reviewed. Policy must be interpreted. Exceptions must be justified.

At this stage, the limiting factor is no longer sourcing activity. It is the speed and consistency of decision-making.

Decision velocity determines:

- How quickly borrowers receive approvals

- How efficiently credit committees operate

- How many deals analysts can realistically handle

- Whether strong borrowers remain engaged

When decision velocity lags, pipeline growth becomes self-defeating. More deals simply mean longer queues.

Where Analysts Lose Time Today

Credit desks rarely slow down because of lack of effort. They slow down because of structural friction. Several recurring bottlenecks appear across institutions:

1. Manual Financial Spreading

Income statements, balance sheets, and tax returns arrive in inconsistent formats. Analysts spend hours rekeying line items, reconciling totals, adjusting parent-child structures, and validating numbers.

Even small classification differences require review. Multi-entity borrowers amplify the workload. By the time financials are structured for analysis, significant time has already been consumed.

2. Rework Loops

Manual spreading introduces risk of transcription error or inconsistent categorization. When discrepancies surface during underwriting or committee review, files return to analysts for correction.

These rework loops compound:

- Data is adjusted

- Ratios must be recalculated

- Narrative explanations updated

- Reports regenerated

Each loop slows decision velocity.

3. Policy Interpretation Escalations

Analysts frequently pause files to clarify policy applications. Questions may include:

- Is this leverage threshold absolute or adjustable?

- Does this industry fall under concentration limits?

- How have similar exceptions been handled historically?

Escalations to senior staff create queue effects. Repetitive questions increase cost per decision and reduce SME availability for complex risk analysis.

4. Inconsistent Financial Structure

When business financials are categorized differently across deals, portfolio comparisons and ratio calculations become inconsistent. This forces additional manual oversight and slows credit committee review.

In combination, these friction points form the hidden bottleneck.

The Growth Impact of a Slower Credit Desk

When the credit desk becomes the limiting factor, the consequences extend beyond operational inconvenience.

- Borrowers lose confidence due to delayed approvals

- Relationship managers feel friction between sales and underwriting

- High-quality borrowers may seek faster competitors

- Credit teams experience burnout during volume surges

Most importantly, revenue conversion stalls. Pipeline velocity outpaces decision velocity. Institutions may attempt to solve this through hiring. But adding headcount without addressing structural inefficiencies only scales friction.

Subscribe to BeSmartee 's Digital Mortgage Blog to receive:

- Mortgage Industry Insights

- Security & Compliance Updates

- Q&A's Featuring Mortgage & Technology Experts

True growth requires improving how decisions move, not just how deals enter the funnel.

How Structured Financial Spreading Reduces Rework

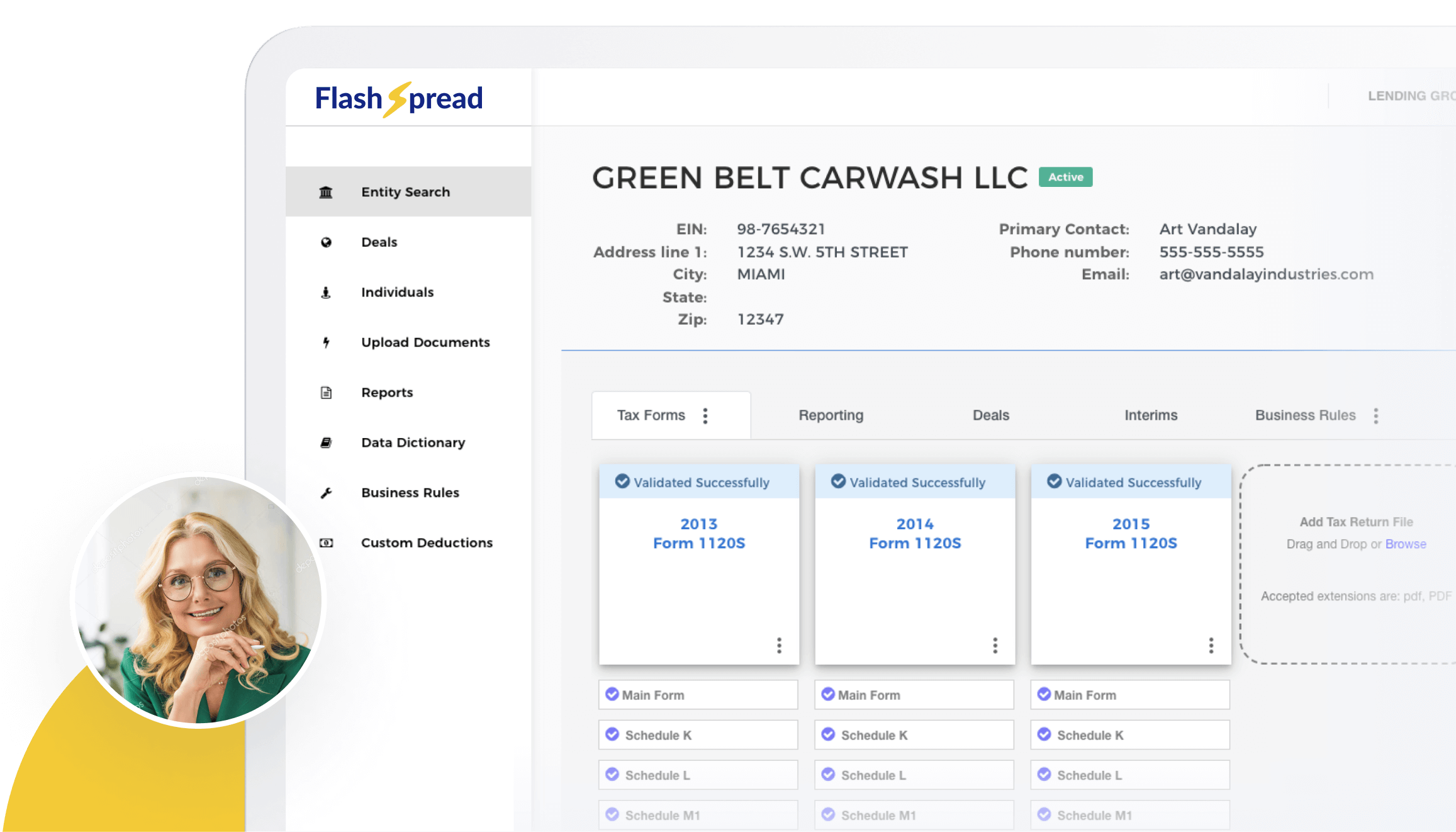

One of the most time-consuming stages in underwriting is transforming borrower documents into structured financial data.

FlashSpread addresses this bottleneck directly by applying advanced OCR and machine learning to extract and organize financial data from tax returns, income statements, and balance sheets. Instead of relying solely on manual rekeying, analysts receive structured, normalized data that is ready for review.

This reduces friction in several ways:

- Less time spent on transcription and reconciliation

- Consistent categorization across borrowers and periods

- Parent-child validation to ensure totals align

- Cleaner inputs for ratio analysis and reporting

When financial data enters underwriting in a standardized structure, downstream review becomes more efficient. Fewer classification inconsistencies mean fewer rework cycles. Ratios are calculated consistently. Comparisons across borrowers become clearer.

Structured spreading does not eliminate analyst oversight. It reduces the manual groundwork that slows them down.

Underwriting Intelligence as a Decision Accelerator

Beyond financial spreading, decision velocity is influenced by how quickly policy questions are resolved.

FlashSpread’s underwriting intelligence layer, AskFlash, supports credit desks by providing AI-powered, source-cited answers drawn directly from institutional credit policies. Analysts can submit questions via chat, SMS, or email and receive contextual responses grounded in approved documentation.

Key capabilities include:

- Multi-policy evaluation of a single question

- Human-in-the-loop escalation for uncertain cases

- Structured capture of SME responses

- Automation of approximately 90 percent of repetitive policy Q&A

This reduces interpretive bottlenecks and ensures consistent application of policy across teams. Instead of waiting for manual clarification, analysts receive timely guidance that keeps deals moving. The result is improved decision velocity without lowering standards.

Q&A: Decision Velocity and Growth

Q: Is faster underwriting risky?

A. Speed alone is not the objective. Structured processes improve both speed and consistency by reducing manual friction and interpretive variability.

Q: Does automation reduce credit rigor?

A. No. Automation reduces repetitive tasks. Final credit decisions remain human-led.

Q: Can decision velocity really impact revenue?

A. Yes. Faster, consistent decisions increase borrower confidence and improve conversion from pipeline to funded volume.

From Cost Center to Growth Lever

Traditionally, the credit desk has been viewed as a necessary operational function, essential but not revenue-generating. However, when structured effectively, underwriting becomes a growth multiplier. By:

- Reducing manual spreading time

- Minimizing rework loops

- Streamlining policy interpretation

- Standardizing financial structure

institutions increase the number of deals they can evaluate without proportionally increasing headcount.

Decision velocity improves. Pipeline conversion strengthens. Borrower experience becomes more competitive. The credit desk shifts from being a bottleneck to being a strategic enabler.

Roundup

Most lenders focus heavily on front-end pipelines. But pipeline growth alone does not produce funded growth. The real constraint in commercial lending is often decision velocity, and that velocity depends on the credit desk.

Manual spreading, inconsistent financial structure, and repetitive policy escalations quietly slow deals. Over time, these bottlenecks limit scalability and revenue conversion. By introducing structured financial spreading and underwriting intelligence, institutions can reduce friction, minimize rework, and accelerate credit decisions without compromising standards.

If your pipeline continues to grow but funded volume does not, it may be time to examine where decisions slow down. Explore how FlashSpread helps credit desks move from documents to decisions with greater speed and consistency.