In commercial lending, risk conversations usually center on credit performance. Default rates. Concentration exposure. Economic volatility. Portfolio monitoring dashboards. But there is another risk building quietly inside many institutions, and it rarely appears in reports. It’s knowledge loss.

As experienced credit officers retire, teams grow, and turnover increases, institutional judgment begins to thin. Not because credit policies disappear. Not because guidelines are undocumented. But because the reasoning behind decisions—the nuance, precedent, interpretation, and risk appetite context—lives inside people. And when people leave, that judgment often leaves with them.

This blog explores why knowledge loss may be one of the most underestimated risks in commercial lending, how it affects underwriting consistency and speed, and why leading institutions are beginning to treat underwriting intelligence as knowledge infrastructure.

Key Insights at a Glance

- Institutional knowledge often lives in individuals, not systems

- Turnover and retirement can weaken underwriting consistency

- Policies capture rules, but not always applied judgment

- Knowledge silos create bottlenecks and delays

- Repetitive credit Q&A increases cost per decision

- Underwriting intelligence preserves expertise and strengthens consistency

The Risk No Dashboard Shows

Credit loss is measurable. Knowledge loss is not. Every institution maintains documented credit policies. Risk ratings are defined. Approval authorities are clear. Exceptions are logged. But daily credit decisions rarely rely on policy text alone. They depend on:

- Interpretation of gray areas

- Historical precedent

- Institutional risk tolerance

- Industry nuance

- Context behind prior exceptions

When a senior underwriter answers a question, they are rarely just quoting policy. They are applying experience layered over policy. When that senior underwriter retires or transitions out, the written document remains, but the interpretive layer weakens.

Over time, this creates subtle but meaningful consequences:

- Slower decision cycles

- Increased escalations

- Inconsistent interpretations

- Higher cost per credit answer

- Reduced confidence among junior analysts

The risk isn’t that policy disappears. It’s that decision intelligence fragments.

Why Credit Desks Feel the Pressure First

Knowledge erosion tends to surface most clearly inside the credit desk.

Commercial credit desks field a high volume of policy-related questions daily. Answers are often buried in knowledge silos, scattered across SharePoint folders, PDF manuals, email threads, disconnected systems, and individual expertise. When analysts cannot quickly locate the right answer:

- They escalate to senior staff

- Decision queues grow

- Interpretation varies by responder

- Turnaround time increases

This leads directly to:

- Bottlenecks and delays

- Inconsistent policy interpretations

- High cost per decision due to manual filtering and fielding

What begins as a knowledge access problem becomes an operational inefficiency and eventually, a competitive disadvantage.

Growth Amplifies Knowledge Risk

Ironically, institutional growth can accelerate knowledge erosion. When lending teams expand:

- New analysts onboard quickly

- Senior SMEs answer more repetitive questions

- Policy interpretation spreads unevenly

- Informal mentorship replaces structured knowledge capture

As credit portfolios grow more complex, policy frameworks expand as well. The more detailed the guidelines, the harder they become to navigate manually.

Even well-documented policies cannot eliminate friction if answers remain difficult to access.

The issue is not document availability. It is answer accessibility.

Policies Capture What Was Written—Not Always How It Was Applied

A credit policy might define minimum DSCR thresholds or industry exposure limits. But it often does not explain:

- When exceptions were historically considered

- How certain industries were treated differently

- How prior edge cases were resolved

- Which qualitative factors carried more weight in practice

Institutional judgment lives between the lines. When that judgment is not structurally captured, two risks emerge:

- Over-conservatism: junior analysts escalate excessively or apply policy rigidly without nuance.

- Inconsistency: interpretations vary by reviewer, creating uneven credit decisions.

Neither outcome strengthens portfolio quality.

Q&A: The Knowledge Risk Leaders Rarely Say Out Loud

Q: Isn’t this just a training issue?

A. Training helps, but static onboarding cannot replicate dynamic judgment built over years. Knowledge must be continuously captured and accessible.

Subscribe to BeSmartee 's Digital Mortgage Blog to receive:

- Mortgage Industry Insights

- Security & Compliance Updates

- Q&A's Featuring Mortgage & Technology Experts

Q: Can’t policies simply be updated more often?

A. Policies define boundaries. They do not eliminate repetitive question flow or capture real-time interpretation.

Q: Does knowledge loss truly affect profitability?

A. Yes. Slower decisions reduce competitiveness. Inconsistent interpretations increase rework and operational cost. Both directly impact revenue and efficiency.

Underwriting Intelligence as Knowledge Infrastructure

If knowledge loss is structural, the response must also be structural.

Leading credit teams are moving beyond static document repositories. They are implementing underwriting intelligence systems that transform fragmented knowledge into searchable, usable infrastructure.

This means:

- Delivering fast, accurate, source-cited answers to policy questions

- Reducing repetitive escalations

- Preserving SME insights through structured capture

- Standardizing interpretation across teams

- Maintaining a full audit trail

Instead of relying on individual memory, underwriting intelligence makes institutional knowledge continuously available and continuously improving.

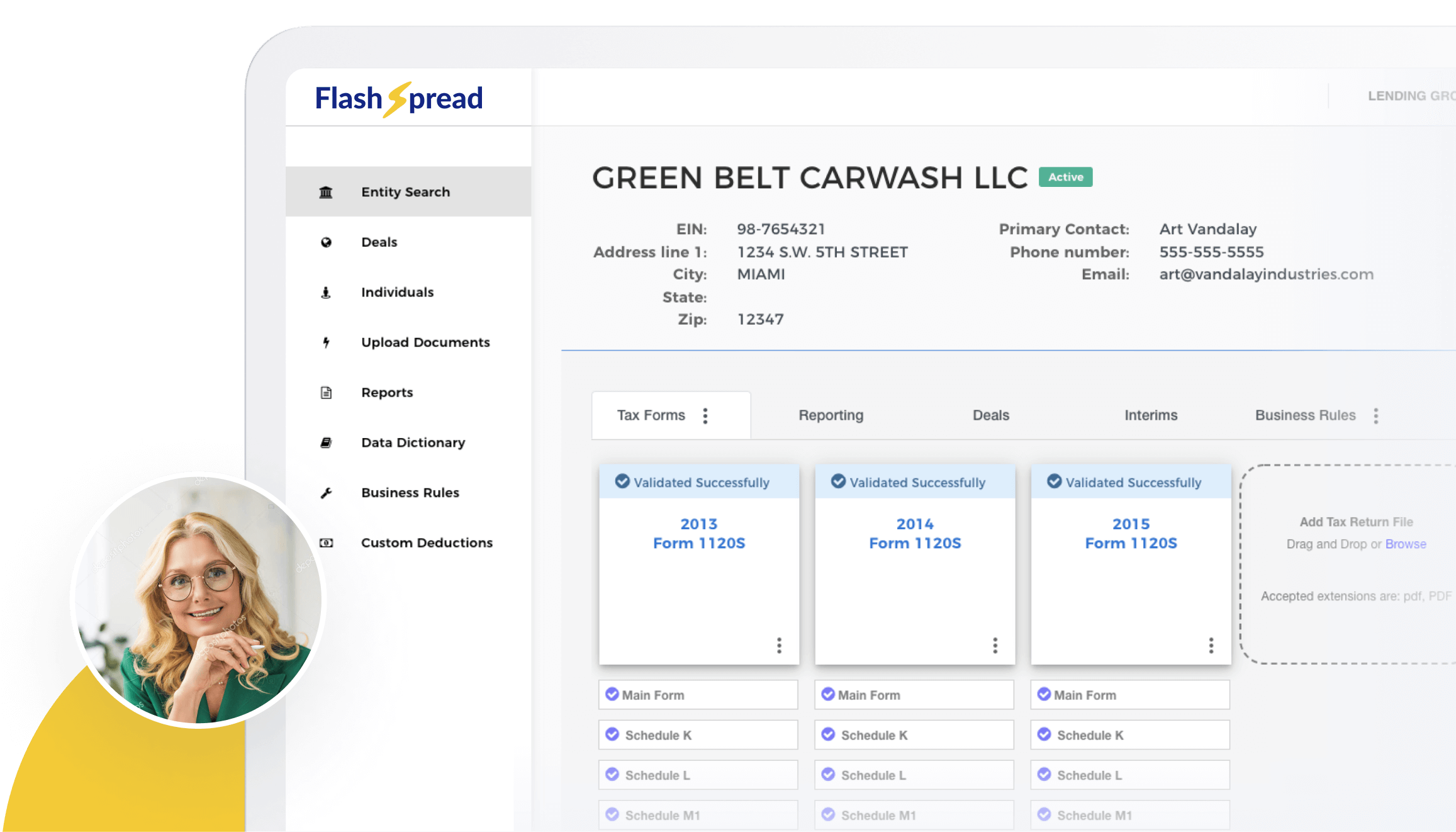

Where FlashSpread Credit Desk Underwriting Intelligence Fits

FlashSpread Credit Desk Underwriting Intelligence is designed specifically to address the knowledge silos and bottlenecks many commercial credit desks face.

It is an AI-powered assistant trained directly on an institution’s credit policies and internal documentation. Analysts and underwriters can ask policy questions via embedded web chat, SMS, or email and receive fast, accurate, source-cited answers drawn from approved content.

Key capabilities include:

- Credit Q&A Assistant delivering context-aware, policy-based responses

- Multi-Policy Decisioning that evaluates a question across multiple guidelines instantly

- Human-in-the-Loop Escalation that routes unknowns to the appropriate SME, captures their response, and learns from it

- Bulk Scenario Testing to validate hundreds of policy scenarios for audits or QA

- Role-Based Tuning to adjust answer depth and tone by user

By automating approximately 90% of repetitive policy Q&A, institutions can significantly lower cost per answer while preserving consistency and nuance.

Implementation is structured for minimal disruption. Institutions can connect policy sources such as SharePoint, Google Drive, or WordPress, normalize guidelines for consistency and reliability, and deploy answer delivery through chat, SMS, or email, often going live in weeks. Importantly, this is not about replacing human judgment. It is about capturing it, preserving the interpretive layer of underwriting intelligence so it remains accessible even as teams evolve.

Knowledge Preservation Is Risk Management

Credit risk will always be modeled and monitored. But institutional capability deserves equal attention. When underwriting knowledge is:

- Accessible

- Structured

- Source-traceable

- Continuously captured

Institutions reduce variability and strengthen long-term consistency. Knowledge preservation ensures:

- New analysts ramp faster

- Decision cycles shorten

- Escalations decrease

- Senior expertise is not lost during turnover

- Growth does not dilute credit quality

Underwriting intelligence becomes more than an operational tool. It becomes risk infrastructure.

Roundup

Credit loss will always command attention. Portfolio dashboards will continue to measure exposure and performance. But knowledge loss is quieter. It happens gradually, through retirements, turnover, and expanding teams.

When institutional judgment remains trapped inside individuals or scattered across documents, credit desks slow down, inconsistencies increase, and operational cost rises.

Treating underwriting intelligence as infrastructure changes that trajectory. By delivering fast, source-cited policy answers and capturing interpretive expertise over time, institutions preserve judgment instead of losing it.

If knowledge loss is a risk your institution has not yet measured, it may be time to rethink how underwriting intelligence is structured. Explore how FlashSpread helps credit teams transform institutional knowledge into lasting infrastructure.